For many families, the home is the most valuable asset they own. As property values rise, some homeowners start looking for ways to reduce potential estate taxes while still keeping the ability to live in their home. One tool sometimes used in advanced estate planning is a Personal Residence Trust, often structured as a Qualified Personal Residence Trust (QPRT).

A Personal Residence Trust is a strategy that allows a homeowner to transfer their residence to a trust while retaining the right to live in the property for a fixed period of time. If structured properly, this can significantly reduce the taxable value of the home for estate tax purposes.

However, this strategy is not for everyone. It involves trade-offs and risks that need to be carefully considered.

Let’s walk through how it works.

What Is a Personal Residence Trust?

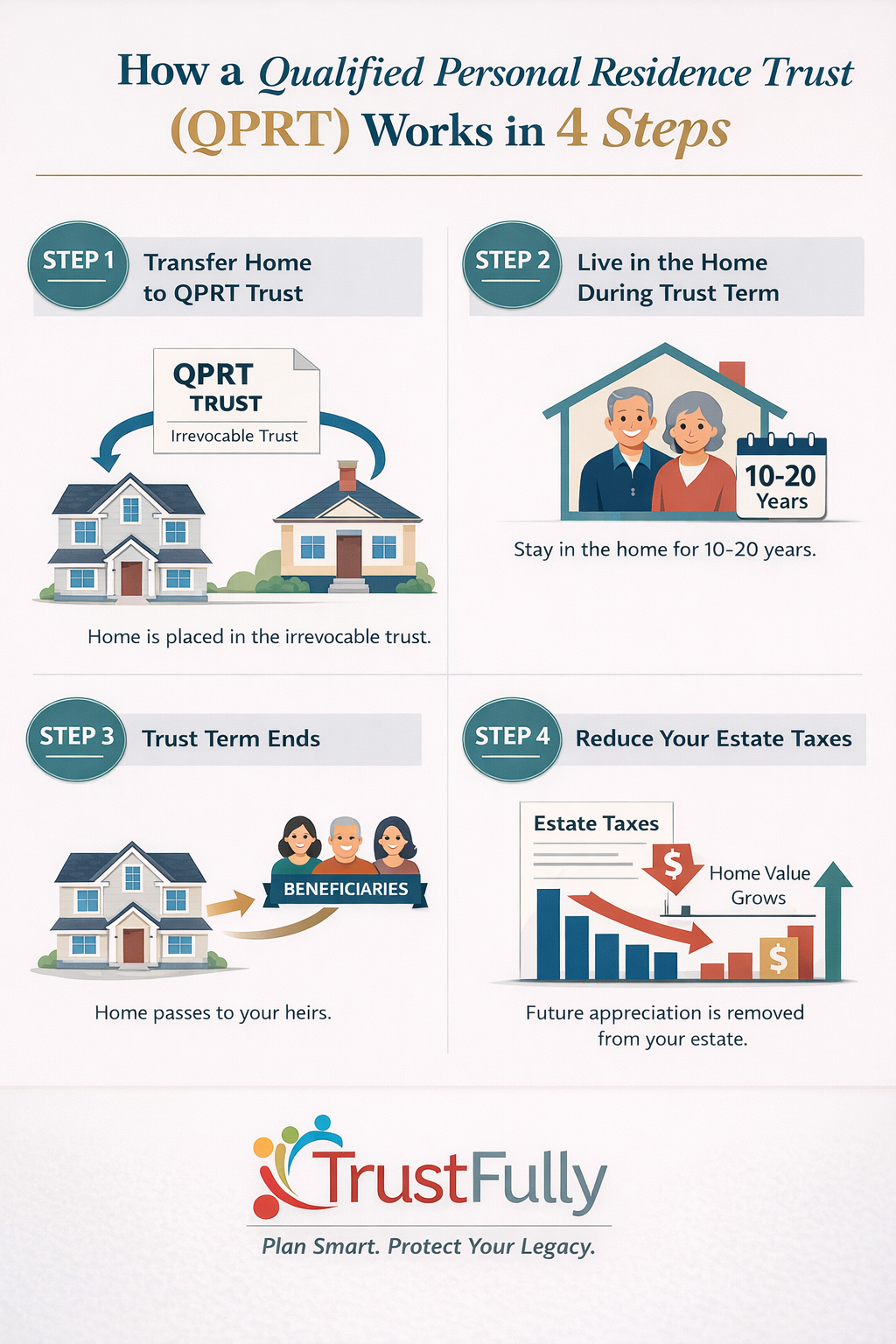

A Personal Residence Trust (PRT) is an irrevocable trust designed specifically to hold a personal residence. The homeowner transfers the property into the trust but keeps the right to live in the home for a predetermined number of years.

During that retained period, the homeowner continues to live in the property just as they did before the transfer.

At the end of that period, ownership of the home passes to the trust beneficiaries—often children or other family members.

The key benefit is that the transfer is treated as a gift of the future value of the home, not the full current value.

How a QPRT Reduces Estate Taxes

The tax benefit comes from the way the IRS values the gift.

When you transfer a home to a QPRT, the value of the gift is discounted because you retain the right to live in the property for a set number of years.

In other words, your children are not receiving the home today. They are receiving the right to own the home in the future.

Because of that delay, the IRS calculates a lower present value for the gift.

If the homeowner survives the trust term, the home passes to the beneficiaries outside the estate.

This means the future appreciation of the property is also removed from the estate, which can significantly reduce estate taxes for high-value estates.

Example

Suppose a home is worth $1,000,000 today.

A homeowner transfers the property into a 15-year QPRT but keeps the right to live there during that period.

Because the homeowner retains that right, the IRS might value the gift at $400,000 instead of $1,000,000 (exact numbers depend on IRS calculations and interest rates).

If the homeowner survives the 15-year term and the house is worth $1.8 million at that time, the entire property passes to the beneficiaries outside the estate.

That appreciation would not be subject to estate tax.

What Happens After the Trust Term Ends?

Once the QPRT term expires, the beneficiaries become the owners of the property.

In many cases, the original homeowner continues to live in the house but must now pay rent to the beneficiaries.

While that may sound unusual, it actually provides an additional estate planning benefit. Paying rent to family members transfers more wealth out of the estate without being treated as a gift.

The Major Risk: Surviving the Trust Term

The biggest risk with a Personal Residence Trust is simple.

The homeowner must outlive the trust term.

If the homeowner dies before the term expires, the property is pulled back into the estate and the tax benefits are largely lost.

For this reason, selecting the length of the trust term requires careful planning.

A longer term produces a larger tax discount, but also increases the risk that the homeowner will not survive the term.

Other Limitations of a Personal Residence Trust

While a QPRT can be a powerful strategy, it has several practical limitations.

First, the trust is irrevocable. Once the property is transferred into the trust, the homeowner cannot simply undo the transfer.

Second, the property must remain a personal residence. If the home is sold, the trust must follow specific rules about how the proceeds are handled.

Third, beneficiaries will not receive a step-up in tax basis when the homeowner dies if the home has already transferred outside the estate. This can create capital gains tax considerations if the property is sold later.

For these reasons, QPRTs are usually used only in larger estates where potential estate taxes outweigh these trade-offs.

Who Typically Uses a QPRT?

Personal Residence Trusts are most commonly used by homeowners who:

- Have significant real estate value

- Are concerned about future estate taxes

- Expect the home to appreciate significantly

- Want to transfer wealth to children or family members

For many families, simpler estate planning tools—such as revocable living trusts, beneficiary deeds, or transfer-on-death planning—may be more appropriate.

Is a Personal Residence Trust Right for You?

A Personal Residence Trust can be an effective way to move a valuable home out of your estate while continuing to live there for years.

But it is also a strategy that requires careful analysis of tax rules, life expectancy considerations, and long-term planning goals.

Because the trust is irrevocable and the tax rules are complex, it should always be designed with experienced estate planning guidance.

Planning Your Estate the Right Way

Estate planning is not one-size-fits-all. Some families need sophisticated tax strategies, while others simply need a clear plan that avoids probate and protects their loved ones.

If you want to explore what type of estate plan makes the most sense for your situation, speaking with an experienced attorney can help you understand your options and avoid costly mistakes.

Comments are closed