Saving for a child’s education can feel overwhelming. Tuition costs continue to rise, and many parents and grandparents want to help without sacrificing their own financial stability.

One of the most commonly used tools for education savings in the United States is the 529 college savings plan. These accounts offer significant tax advantages and flexibility, which is why they have become a central part of many families’ financial planning strategies.

But like any financial tool, 529 plans come with both benefits and limitations. Understanding how they work can help you decide whether a 529 plan fits into your overall financial and estate planning goals.

What Is a 529 Plan?

A 529 plan is a tax-advantaged savings account designed specifically to help families save for education expenses.

The plans are named after Section 529 of the Internal Revenue Code, which created these accounts to encourage long-term education savings.

529 plans are typically sponsored by states, but you are not limited to your home state’s plan. Most families can invest in any state’s plan.

There are two general types of 529 plans:

College Savings Plans

These function similarly to investment accounts. Contributions are invested in mutual funds or similar portfolios, and the value grows over time.

Prepaid Tuition Plans

These allow families to prepay tuition at participating institutions at today’s prices.

Most families use college savings plans, which provide more flexibility.

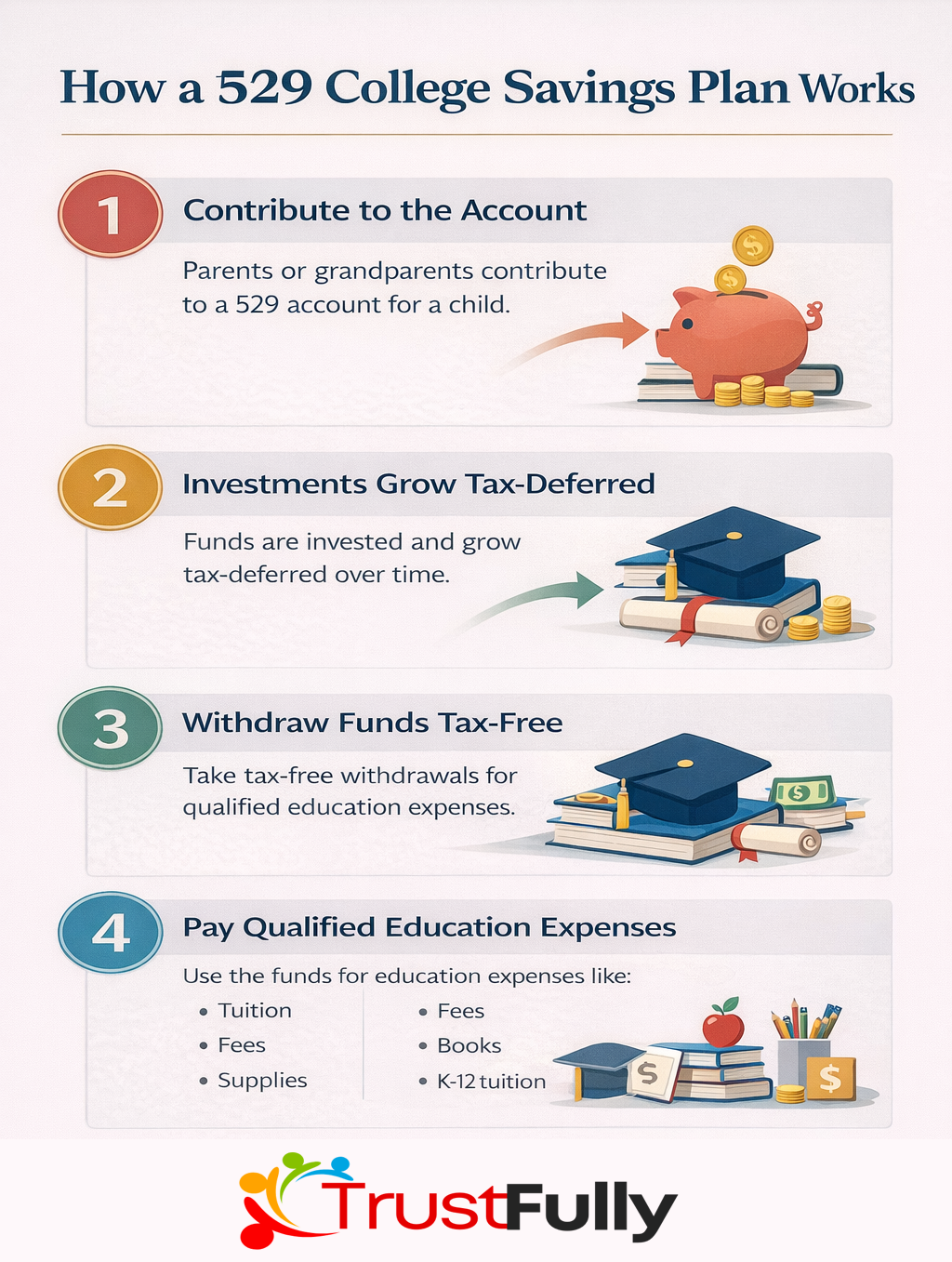

How a 529 Plan Works

A 529 plan is relatively simple.

An account owner contributes money into the account and names a beneficiary, usually a child or grandchild.

The funds are then invested and grow tax-deferred.

When the money is withdrawn for qualified education expenses, the withdrawals are generally tax-free.

Qualified expenses may include:

- Tuition

- Fees

- Books

- Required supplies

- Certain housing expenses

- Computers and related technology

Recent changes in federal law have also expanded how 529 funds can be used.

529 plans can now be used for up to $10,000 per year for K-12 tuition and may also be used for certain apprenticeship programs.

The Tax Advantages of 529 Plans

One of the biggest reasons families use 529 plans is their tax treatment.

Tax-Free Growth

Investment earnings grow tax-deferred, meaning you do not pay taxes each year on gains inside the account.

Tax-Free Withdrawals

If the funds are used for qualified education expenses, the withdrawals are not subject to federal income tax.

Potential State Tax Benefits

Many states offer state tax deductions or credits for contributions to their own 529 plan.

Missouri residents, for example, may receive a state income tax deduction for contributions to the Missouri MOST 529 plan.

Estate Planning Benefits of 529 Plans

529 plans can also play a useful role in estate planning.

When someone contributes to a 529 plan, the contribution is treated as a completed gift for gift tax purposes. This means the assets are generally removed from the contributor’s estate. However, the contributor retains control over the account, which is unusual compared to most gifting strategies.

For example, the account owner can:

- Change the beneficiary

- Decide when withdrawals occur

- Maintain investment control

There is also a special rule that allows contributors to front-load up to five years of gift tax exclusions at once.

This means a grandparent could contribute a very large amount to a grandchild’s 529 plan without triggering gift tax consequences, depending on current annual exclusion limits.

Potential Drawbacks of 529 Plans

Although 529 plans are powerful tools, they are not perfect.

Limited Use of Funds

Withdrawals must generally be used for qualified education expenses. If funds are used for non-qualified purposes, earnings may be subject to income tax and penalties.

Investment Risk

Because most 529 plans invest in market-based portfolios, account values can rise or fall depending on market performance.

Financial Aid Impact

529 accounts owned by parents may be considered assets when calculating financial aid eligibility.

However, they are typically treated more favorably than accounts owned directly by the student.

Overfunding Risk

If the beneficiary does not attend college or receives significant scholarships, excess funds could remain in the account.

Recent changes to federal law now allow some unused 529 funds to be rolled into a Roth IRA for the beneficiary, subject to certain limitations, which may reduce this concern.

When a 529 Plan Makes Sense

A 529 plan may be a strong option for families who:

- Expect to pay for higher education

- Want tax-advantaged investment growth

- Are saving long term for a child or grandchild

- Want a flexible way to gift education funds

However, a 529 plan should usually be considered alongside other planning tools, including retirement planning and broader estate planning strategies.

How 529 Plans Fit Into a Larger Estate Plan

Education savings should be viewed as part of a broader financial and estate plan.

Families often combine 529 plans with other tools such as:

- Revocable living trusts

- beneficiary designations

- education gifts from grandparents

You can learn more about these strategies in our related articles:

- What Happens If You Die Without an Estate Plan

- How to Properly Fund Your Trust

- Why Parents Should Update Their Estate Plan Every 3–5 Years

Proper planning can ensure that education savings work together with the rest of your estate plan rather than creating unintended complications.

Final Thoughts

529 plans can be one of the most effective tools available for saving for education. Their tax advantages, flexibility, and estate planning benefits make them attractive to many families.

However, they are only one piece of a larger financial strategy. Understanding how they interact with taxes, estate planning, and financial aid considerations is essential before committing significant funds.

If you are building a long-term financial plan for your family, it can be helpful to review how education savings strategies fit into your broader estate plan.

We Can Help Guide You On Ways To Invest In Your Family’s Future

Set up a free consultation, and we can help you help your family. ‘

Comments are closed